Institute of Actuaries of India 2010 CT-7 Economics Core Technical ( ) - Question Paper

INSTITUTE OF ACTUARIES OF INDIA

EXAMINATIONS 14th May 2010 Subject CT7 - Business Economics Time allowed: Three Hours (10.00 to 13.00 Hrs)

Total Marks: 100

INSTRUCTIONS TO THE CANDIDATES

1) Please read the instructions on the front page of answer booklet and instructions to examinees sent along with hall ticket carefully and follow without exception

2) Mark allocations are shown in brackets.

3) Attempt all questions, beginning your answer to each question on a separate sheet. However, answers to objective type questions could be written on the same sheet.

4) In addition to this paper you will be provided with graph paper, if required.

Q. 1) In a perfectly competitive industry where there are no external benefits from consumption and marginal social cost (MSC) is greater than marginal cost (MC), provision of subsidies will

A. Control overproduction

B. Enhance overproduction

C. Control underproduction

D. Enhance underproduction [1.5] Q. 2) Collusive tendering for a public road project may result in:

A. Higher government expenditure on road

B. Lower government expenditure on road

C. Competitive tendering process

D. Better utilization of government funds [1.5] Q. 3) Tie-in-sales

A. Reduce consumer choices

B. Increases consumer choices

C. Increase consumer surplus

D. Best represent distribution strategy of companies [1.5]

Q. 4) Country A, as compared to Country B, has a lower opportunity cost of producing commodity X and Country B, as compared to Country A, has a lower opportunity cost of producing commodity Y. Thus,

I. It will always be beneficial for country A to export commodity X to country B and import commodity Y from country B

II. It will always be beneficial for country B to export commodity Y to country A and import commodity X from country A

A. Only (I) is untrue

B. Only (II) is untrue

C. Both (I) and (II) are necessarily untrue

D. Both may be true depending on exchange ratio between commodity X and Y [1.5] Q. 5) In a free market, social efficiency may not be achieved because:

A. Social cost is greater than social benefit

B. Private benefit is greater than private cost

C. Private benefit is equal to private cost

Q. 6) If there is balance on capital account and deficit on current account,

A. Balance on capital account will always compensate for deficit on current account and hence ensure overall balance of payments

B. There is no connection between current and capital account in the overall balance of payments

C. There will always be surplus on overall balance of payments

D. Overall balance of payments will always be zero [1.5]

Q. 7) Balance on trade in goods and services (which have price elastic demand)between India and Japan, assumed to be the key trade partners, is likely to increase for India if

A. Inflation rate in India is higher than that in Japan

B. Indian economy grows faster than the Japanese economy

C. Indian Rupee depreciates against Japanese Yen

D. Indian Rupee appreciates against Japanese Yen [1.5]

Q. 8) If GNP at Market Price is greater than GDP at Market Price for India,

A. Value of exports of goods from India is larger than the value of imports of goods into India

B. Net capital flows into India is positive

C. Net capital flows into India is negative

D. Net factor income from abroad for India is positive [1.5]

Q. 9) Suppose an economy is currently in equilibrium and marginal propensity to consume domestically produced goods is 0.80. Decrease in government expenditure by 20 million will lead to:

A. Decrease in equilibrium national income by 20 million

B. Decrease in equilibrium national income by 100 million

C. Increase in equilibrium national income by 20 million

D. Increase in equilibrium national income by 80 million

Q. 10) Gambling is demerit goods because:

A. Private costs are undervalued

B. External costs are overvalued

C. Private cost is overvalued

D. Both private and external costs are overvalued [1.5]

According Keynesian Consumption Function, if current Average Propensity to Save of an individual is 0.30 and his income increases by Rs. 10,000, which of the following statements is most likely to be true?

A. His consumption will increase by Rs. 7,000

Q. 11)

B. His consumption will increase by Rs. 10,000

C. His consumption will decrease by Rs. 3,000

D. His consumption will increase by Rs. 6,500

[1.5]

Which of the following is not a case of equilibrium unemployment?

Q. 12)

A. Unemployment caused by a change in the structure of the industry because of change in demand for a product

B. Unemployment caused by seasonal fluctuation in demand for labour

C. Unemployment resulting from inflexible wages

D. Unemployment due to introduction of labour-saving technology

[1.5]

If aggregate demand curve and aggregate supply curve simultaneously shift towards right:

Q. 13)

A. Equilibrium price level will necessarily increase

B. Equilibrium price level will necessarily decrease

C. Equilibrium national income will necessarily increase

D. Equilibrium national income will necessarily decrease [1.5] If unemployment has fallen and inflation has stabilized,

Q. 14)

A. Phillips curve is upward sloping

B. Phillips curve is vertical straight line

C. Phillips curve is inverted U-shaped

D. Phillips curve is almost horizontal [1.5] Unemployment problem, as an economist might view it, in a given society refers to :

Q. 15)

A. People not willing to take up available jobs - since theyre waiting for better opportunities.

B. People not getting jobs despite their willingness to work.

C. 5 people are doing a job that can be managed by 2 people only.

D. All of the above [1.5]

Q. 16) Mr. Gupta is a Chartered Accountant working in India. He is drawing a salary of 5X. His opportunity cost of employment is :

A. The salary drawn by Mr. Sharma who works at the same level as Mr. Gupta in the current organization

B. The salary that Mr. Gupta would be able to obtain, if he switches jobs, based on salary surveys conducted by a reputed HR firm

C. The salary mentioned in Mr. Guptas offer letter, which he got from a close competitor last week

D. The salary that Mr. Gupta can obtain if he moves to Saudi Arabia, since there is

a huge demand for accountants in that country. [1.5]

Q. 17) Demand Curve :

Price of Good X

Quantity Demanded of Good Y

Looking at the demand curve, we can say that:

A. Good X is a close substitute of Good Y -

B. Good X is a poor substitute of Good Y

C. Good X is a close complementary good for Good Y

D. Good Y is a Giffen good

[1.5]

Q. 18) Short Run Average Variable Cost is minimum when :

A. Short Run Marginal Cost is Maximum

B. Short Run Marginal Cost is Minimum

C. When Short Run Total Cost is Minimum

D. When Short Run Average Variable Costs equals Short Run Marginal Cost [1.5]

Q. 19) Economies of Scale occur due to :

A. Constant Returns to scale and constant factor costs

B. Constant Returns to scale and increasing factor costs

C. Increasing returns to scale and constant factor costs

D. Increasing Returns to scale and increasing factor costs

[1.5]

Q. 20) Consumer Surplus is negative for :

A. Where Customers are not given value for money

B. Inferior (Giffen) goods

C. Demand is perfectly Price Inelastic

D. Demand is perfectly Price Elastic [1.5]

Q. 21) Good A has a high (and negative) cross price elasticity of demand with respect to Good B What pricing strategy could be beneficial?

A. Cost-based pricing

B. Limit Pricing

C. Discriminatory Pricing

D. Full Range Pricing [1.5]

Q. 22) In the short run, if the firm experiencing constant returns to variable factor, then :

A. Marginal Cost equals Average Variable Cost

B. Marginal Costs and Average Variable Cost are constant

C. Marginal Costs and Average Cost are constant

D. Average Variable Costs and Total Cost are falling. [1.5]

Q. 23) The demand for term assurance, in India, is expected to be :

A. Infinitely Price Inelastic

B. Highly Price Inelastic

C. Highly Price Elastic

D. Infinitely Price Elastic [1.5]

Q. 24) Under perfect competition :

A. Industry and Firm have infinitely elastic Demand Curves

B. Industry alone has infinitely elastic Demand Curve

C. Firm alone has infinitely elastic Demand Curve

Q. 25) Consumer M has a higher income than consumer N but they have identical preferences and pay the same prices for the goods which they consume. If they are both utility maximisers then:

A. The marginal utility from each good consumed will be higher for M than for N and M will have a higher total utility.

B. The marginal utility from each good consumed will be higher for M than for N and M will have a lower total utility.

C. The marginal utility from each good consumed will be lower for M than for N and M will have a higher total utility.

D. The marginal utility from each good consumed will be lower for M than for N

and M will have a lower total utility. [1.5]

Q. 26) A perfectly competitive firm is producing at a level of output for which short run marginal cost exceeds marginal revenue. What should the firm do to maximise its short run profits?

A. raise its price

B. reduce its price

C. raise its output

D. reduce its output [1.5]

Q. 27) The time dimension of market adjustment principle suggests :

I. Small short-run quantity change and larger long-run quantity change

II. Small short-run price change and larger long-run price change

III. Large short-run quantity change and smaller long-run quantity change

IV. Large short-run price change and smaller long-run price change

A. I & II

B. I & IV

C. II & III

D. None of the above

[1.5]

Q. 28) Constant returns to scale means that as a firms scale of production is increased:

A. Long run total costs remain constant

B. Total output remains unchanged

C. Long run average costs and long run marginal costs are equal

D. Fixed costs remain constant [1.5]

Q. 29) Perfectly Contestable Markets means that :

A. There are significant entry and exit costs

B. Free and Costless entry and exit

C. Lack of Monopoly

D. Lack of Collusive Oligopoly [1.5]

Q. 30) Which of these is NOT one of the four possible strategies in a growth vector matrix?

A. market penetration

B. market saturation

C. market development

D. product development [1.5] Q. 31) Following table contains some national income related facts about an economy.

|

[Rs. Crore] | ||||||||||||||||||||||

|

Calculate the value of Net Indirect Taxes (Indirect Taxes - Subsidies).

[8]

Q. 32) An economy is characterized by following equations:

C = 100 + cYd =100 + 0.75Yd,

I = 45,

G = 80,

T = 20 + 0.20Y,

R = 40,

X = 40,

M = 30 + 0.10Y,

where C is consumption function, c is marginal propensity to consume, Yd is

Disposable income (Y - T + R), I is autonomous investment, G is autonomous government purchases, T is tax function, Y is level of income, R is autonomous transfer payments by the government, X is autonomous exports, M is import function.

a) Find out equilibrium national income. (5)

b) What will be the size of Government Purchases multiplier? (3)

c) Other things remaining same, by what amount the government purchases should increase in order to raise the equilibrium national income by 20%? (3)

|

Given the following information, | |||||

|

a) Which country has absolute cost advantage in production of pens? (2)

Q. 33)

b) Which country has comparative advantage in production of Audio tape recorders? (2)

c) If Japan offers one audio tape recorder for 17.5 pens, should India accept the offer? (2)

[6]

What is natural level of unemployment? What are its causes? What policies do you suggest to deal with this problem? [3]

Q. 34)

Q. 35)

Q. 36) Q. 37)

Distinguish between a dominant equilibrium and a Nash equilibrium. [3]

How is the short-run supply curve of a perfectly competitive firm determined? [5]

a) List the 3 models used for describing the rival behavior on non-collusive ligopoly? (1)

b) What are the key underlying assumptions for the kinked demand theory (2)

[3]

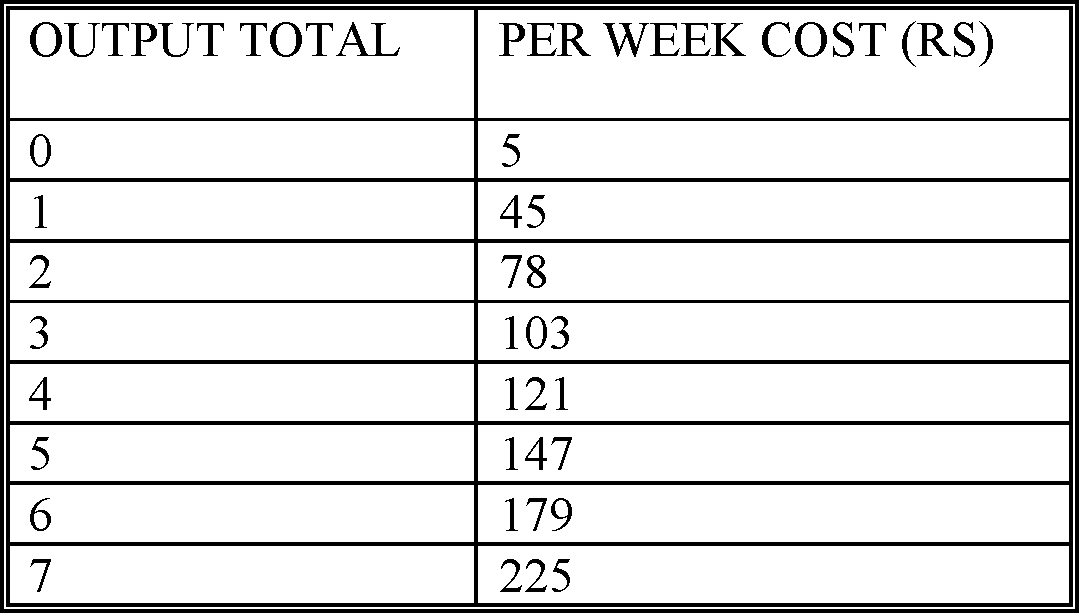

Consider the following data for a perfectly competitive firm, where the market Price for the commodity is Rs.32:

(i) Construct a table showing the marginal cost and average variable cost at each level of output.

(2)

(1)

(1)

[4]

(ii) Calculate the profit maximising level of output for the firm.

(iii) Calculate the profit at the profit maximising level of output.

Q. 39) Consider the following payoff matrix for two firms, A and B. The payoffs show the profit resulting from various combinations of low-price and high-price strategies.

|

Firm B | |||

|

High Price |

Low Price | ||

|

Firm A |

High Price |

50,50 |

10,80 |

|

Low Price |

80,10 |

20,20 | |

(i) Which strategy would maximise joint profit? (1)

(ii) What is the dominant strategy for each firm? (2)

(iii)What happens to the payoff table if Firms A and B introduce a meet-the-competition clause into their contracts with customers? (1)

(iv)Which strategy would firms choose in this situation? (1)

[5]

Q. 40) Discuss Limit pricing with the help of a diagram [3]

Q. 41) a. Define Mergers and Takeovers. (1)

b. Differentiate between the two (1.5)

c. Discuss the types of mergers. (1.5)

[4]

Page 10 of 10

INSTITUTE OF ACTUARIES OF INDIA

EXAMINATIONS 14th May 2010 Subject CT7 - Business Economics Time allowed: Three Hours (10.00 to 13.00 Hrs)

Total Marks: 100

INSTRUCTIONS TO THE CANDIDATES

1) Please read the instructions on the front page of answer booklet and instructions to examinees sent along with hall ticket carefully and follow without exception

2) Mark allocations are shown in brackets.

3) Attempt all questions, beginning your answer to each question on a separate sheet. However, answers to objective type questions could be written on the same sheet.

4) In addition to this paper you will be provided with graph paper, if required.

Q. 1) In a perfectly competitive industry where there are no external benefits from consumption and marginal social cost (MSC) is greater than marginal cost (MC), provision of subsidies will

A. Control overproduction

B. Enhance overproduction

C. Control underproduction

D. Enhance underproduction [1.5] Q. 2) Collusive tendering for a public road project may result in:

A. Higher government expenditure on road

B. Lower government expenditure on road

C. Competitive tendering process

D. Better utilization of government funds [1.5] Q. 3) Tie-in-sales

A. Reduce consumer choices

B. Increases consumer choices

C. Increase consumer surplus

D. Best represent distribution strategy of companies [1.5]

Q. 4) Country A, as compared to Country B, has a lower opportunity cost of producing commodity X and Country B, as compared to Country A, has a lower opportunity cost of producing commodity Y. Thus,

I. It will always be beneficial for country A to export commodity X to country B and import commodity Y from country B

II. It will always be beneficial for country B to export commodity Y to country A and import commodity X from country A

A. Only (I) is untrue

B. Only (II) is untrue

C. Both (I) and (II) are necessarily untrue

D. Both may be true depending on exchange ratio between commodity X and Y [1.5] Q. 5) In a free market, social efficiency may not be achieved because:

A. Social cost is greater than social benefit

B. Private benefit is greater than private cost

C. Private benefit is equal to private cost

Q. 6) If there is balance on capital account and deficit on current account,

A. Balance on capital account will always compensate for deficit on current account and hence ensure overall balance of payments

B. There is no connection between current and capital account in the overall balance of payments

C. There will always be surplus on overall balance of payments

D. Overall balance of payments will always be zero [1.5]

Q. 7) Balance on trade in goods and services (which have price elastic demand)between India and Japan, assumed to be the key trade partners, is likely to increase for India if

A. Inflation rate in India is higher than that in Japan

B. Indian economy grows faster than the Japanese economy

C. Indian Rupee depreciates against Japanese Yen

D. Indian Rupee appreciates against Japanese Yen [1.5]

Q. 8) If GNP at Market Price is greater than GDP at Market Price for India,

A. Value of exports of goods from India is larger than the value of imports of goods into India

B. Net capital flows into India is positive

C. Net capital flows into India is negative

D. Net factor income from abroad for India is positive [1.5]

Q. 9) Suppose an economy is currently in equilibrium and marginal propensity to consume domestically produced goods is 0.80. Decrease in government expenditure by 20 million will lead to:

A. Decrease in equilibrium national income by 20 million

B. Decrease in equilibrium national income by 100 million

C. Increase in equilibrium national income by 20 million

D. Increase in equilibrium national income by 80 million

Q. 10) Gambling is demerit goods because:

A. Private costs are undervalued

B. External costs are overvalued

C. Private cost is overvalued

D. Both private and external costs are overvalued [1.5]

According Keynesian Consumption Function, if current Average Propensity to Save of an individual is 0.30 and his income increases by Rs. 10,000, which of the following statements is most likely to be true?

A. His consumption will increase by Rs. 7,000

Q. 11)

B. His consumption will increase by Rs. 10,000

C. His consumption will decrease by Rs. 3,000

D. His consumption will increase by Rs. 6,500

[1.5]

Which of the following is not a case of equilibrium unemployment?

Q. 12)

A. Unemployment caused by a change in the structure of the industry because of change in demand for a product

B. Unemployment caused by seasonal fluctuation in demand for labour

C. Unemployment resulting from inflexible wages

D. Unemployment due to introduction of labour-saving technology

[1.5]

If aggregate demand curve and aggregate supply curve simultaneously shift towards right:

Q. 13)

A. Equilibrium price level will necessarily increase

B. Equilibrium price level will necessarily decrease

C. Equilibrium national income will necessarily increase

D. Equilibrium national income will necessarily decrease [1.5] If unemployment has fallen and inflation has stabilized,

Q. 14)

A. Phillips curve is upward sloping

B. Phillips curve is vertical straight line

C. Phillips curve is inverted U-shaped

D. Phillips curve is almost horizontal [1.5] Unemployment problem, as an economist might view it, in a given society refers to :

Q. 15)

A. People not willing to take up available jobs - since theyre waiting for better opportunities.

B. People not getting jobs despite their willingness to work.

C. 5 people are doing a job that can be managed by 2 people only.

D. All of the above [1.5]

Q. 16) Mr. Gupta is a Chartered Accountant working in India. He is drawing a salary of 5X. His opportunity cost of employment is :

A. The salary drawn by Mr. Sharma who works at the same level as Mr. Gupta in the current organization

B. The salary that Mr. Gupta would be able to obtain, if he switches jobs, based on salary surveys conducted by a reputed HR firm

C. The salary mentioned in Mr. Guptas offer letter, which he got from a close competitor last week

D. The salary that Mr. Gupta can obtain if he moves to Saudi Arabia, since there is

a huge demand for accountants in that country. [1.5]

Q. 17) Demand Curve :

Price of Good X

Quantity Demanded of Good Y

Looking at the demand curve, we can say that:

A. Good X is a close substitute of Good Y -

B. Good X is a poor substitute of Good Y

C. Good X is a close complementary good for Good Y

D. Good Y is a Giffen good

[1.5]

Q. 18) Short Run Average Variable Cost is minimum when :

A. Short Run Marginal Cost is Maximum

B. Short Run Marginal Cost is Minimum

C. When Short Run Total Cost is Minimum

D. When Short Run Average Variable Costs equals Short Run Marginal Cost [1.5]

Q. 19) Economies of Scale occur due to :

A. Constant Returns to scale and constant factor costs

B. Constant Returns to scale and increasing factor costs

C. Increasing returns to scale and constant factor costs

D. Increasing Returns to scale and increasing factor costs

[1.5]

Q. 20) Consumer Surplus is negative for :

A. Where Customers are not given value for money

B. Inferior (Giffen) goods

C. Demand is perfectly Price Inelastic

D. Demand is perfectly Price Elastic [1.5]

Q. 21) Good A has a high (and negative) cross price elasticity of demand with respect to Good B What pricing strategy could be beneficial?

A. Cost-based pricing

B. Limit Pricing

C. Discriminatory Pricing

D. Full Range Pricing [1.5]

Q. 22) In the short run, if the firm experiencing constant returns to variable factor, then :

A. Marginal Cost equals Average Variable Cost

B. Marginal Costs and Average Variable Cost are constant

C. Marginal Costs and Average Cost are constant

D. Average Variable Costs and Total Cost are falling. [1.5]

Q. 23) The demand for term assurance, in India, is expected to be :

A. Infinitely Price Inelastic

B. Highly Price Inelastic

C. Highly Price Elastic

D. Infinitely Price Elastic [1.5]

Q. 24) Under perfect competition :

A. Industry and Firm have infinitely elastic Demand Curves

B. Industry alone has infinitely elastic Demand Curve

C. Firm alone has infinitely elastic Demand Curve

Q. 25) Consumer M has a higher income than consumer N but they have identical preferences and pay the same prices for the goods which they consume. If they are both utility maximisers then:

A. The marginal utility from each good consumed will be higher for M than for N and M will have a higher total utility.

B. The marginal utility from each good consumed will be higher for M than for N and M will have a lower total utility.

C. The marginal utility from each good consumed will be lower for M than for N and M will have a higher total utility.

D. The marginal utility from each good consumed will be lower for M than for N

and M will have a lower total utility. [1.5]

Q. 26) A perfectly competitive firm is producing at a level of output for which short run marginal cost exceeds marginal revenue. What should the firm do to maximise its short run profits?

A. raise its price

B. reduce its price

C. raise its output

D. reduce its output [1.5]

Q. 27) The time dimension of market adjustment principle suggests :

I. Small short-run quantity change and larger long-run quantity change

II. Small short-run price change and larger long-run price change

III. Large short-run quantity change and smaller long-run quantity change

IV. Large short-run price change and smaller long-run price change

A. I & II

B. I & IV

C. II & III

D. None of the above

[1.5]

Q. 28) Constant returns to scale means that as a firms scale of production is increased:

A. Long run total costs remain constant

B. Total output remains unchanged

C. Long run average costs and long run marginal costs are equal

D. Fixed costs remain constant [1.5]

Q. 29) Perfectly Contestable Markets means that :

A. There are significant entry and exit costs

B. Free and Costless entry and exit

C. Lack of Monopoly

D. Lack of Collusive Oligopoly [1.5]

Q. 30) Which of these is NOT one of the four possible strategies in a growth vector matrix?

A. market penetration

B. market saturation

C. market development

D. product development [1.5] Q. 31) Following table contains some national income related facts about an economy.

|

[Rs. Crore] | ||||||||||||||||||||||

|

Calculate the value of Net Indirect Taxes (Indirect Taxes - Subsidies).

[8]

Q. 32) An economy is characterized by following equations:

C = 100 + cYd =100 + 0.75Yd,

I = 45,

G = 80,

T = 20 + 0.20Y,

R = 40,

X = 40,

M = 30 + 0.10Y,

where C is consumption function, c is marginal propensity to consume, Yd is

Disposable income (Y - T + R), I is autonomous investment, G is autonomous government purchases, T is tax function, Y is level of income, R is autonomous transfer payments by the government, X is autonomous exports, M is import function.

a) Find out equilibrium national income. (5)

b) What will be the size of Government Purchases multiplier? (3)

c) Other things remaining same, by what amount the government purchases should increase in order to raise the equilibrium national income by 20%? (3)

|

Given the following information, | |||||

|

a) Which country has absolute cost advantage in production of pens? (2)

Q. 33)

b) Which country has comparative advantage in production of Audio tape recorders? (2)

c) If Japan offers one audio tape recorder for 17.5 pens, should India accept the offer? (2)

[6]

What is natural level of unemployment? What are its causes? What policies do you suggest to deal with this problem? [3]

Q. 34)

Q. 35)

Q. 36) Q. 37)

Distinguish between a dominant equilibrium and a Nash equilibrium. [3]

How is the short-run supply curve of a perfectly competitive firm determined? [5]

a) List the 3 models used for describing the rival behavior on non-collusive ligopoly? (1)

b) What are the key underlying assumptions for the kinked demand theory (2)

[3]

Consider the following data for a perfectly competitive firm, where the market Price for the commodity is Rs.32:

(i) Construct a table showing the marginal cost and average variable cost at each level of output.

(2)

(1)

(1)

[4]

(ii) Calculate the profit maximising level of output for the firm.

(iii) Calculate the profit at the profit maximising level of output.

Q. 39) Consider the following payoff matrix for two firms, A and B. The payoffs show the profit resulting from various combinations of low-price and high-price strategies.

|

Firm B | |||

|

High Price |

Low Price | ||

|

Firm A |

High Price |

50,50 |

10,80 |

|

Low Price |

80,10 |

20,20 | |

(i) Which strategy would maximise joint profit? (1)

(ii) What is the dominant strategy for each firm? (2)

(iii)What happens to the payoff table if Firms A and B introduce a meet-the-competition clause into their contracts with customers? (1)

(iv)Which strategy would firms choose in this situation? (1)

[5]

Q. 40) Discuss Limit pricing with the help of a diagram [3]

Q. 41) a. Define Mergers and Takeovers. (1)

b. Differentiate between the two (1.5)

c. Discuss the types of mergers. (1.5)

[4]

Page 10 of 10

|

Attachment: |

| Earning: Approval pending. |